You can typically earn more than a bank account by holding short-term U.S. Treasuries. For example, as of January they are netting over 4.1% and guaranteed by the full faith and credit of the US government. The national average 12-month CD rate is less than 2%, and the average savings account is paying less than 1%.

Tines Capital will not charge an advisory fee to help you do this.

Rates will change over time, but this service is designed to be competitive in any interest rate environment.

Existing Tines Capital clients can begin by contacting their advisor.

New clients can get started using the buttons below:

For most of my life, I didn’t think much about the interest rates I was receiving on cash I had in the bank. My savings just sat in a bank earning next to nothing. That was normal, bank savings rates were near zero and there wasn’t much to do about it.

I hope this letter finds you well as the second quarter has now ended, I want to highlight a few important investment concepts that remain crucial to long-term success. Also, with higher interest rates I want to encourage you to make sure your shorter-term savings, emergency funds, and cash-like positions are getting good interest rates. If not, there are some good opportunities available to earn roughly 4-5% annualized on your savings. As always if you would like to discuss your investments, Tines Capital is only a call away.

A Word on 2023 Performance

2023 has been great for many of Tines Capital’s strategies. The most aggressive and largest strategy we offer was up rather dramatically in the first 6 months of 2023. Whether a strategy is up 50% or down 50% my advice is the same. Money that you need soon should be invested in something stable and conservative. Money you don’t need for many years should be invested in something with a higher potential return – which typically means more volatility.

Investment decisions should be based primarily on when you plan to spend the money, not on recent performance – good or bad. Ignoring recent performance is counterintuitive, but study after study shows investors that are patient & consistent tend to do better.

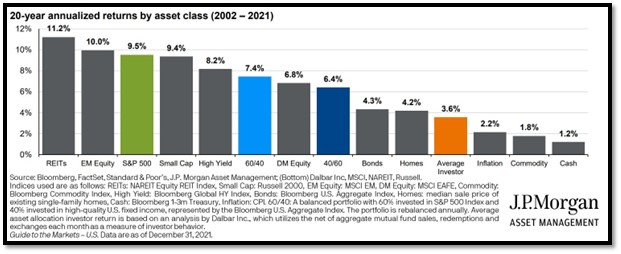

A Study in Patience

The chart below is from a study comparing the average investor return vs. several investment options over a 20-year period. The average investor (orange) had an annualized return of only 3.6%. That is terrible!

Investors did poorly because they tended to pile into an asset based on good recent performance then flee after a bad period. Likewise, investors tended to remain in cash anticipating crashes and often had to watch long bull runs take place mostly without them. The difference is even starker when you convert those annualized returns into overall growth as I have done below.

Ending Value for $10,000 Investment after 20 years.

Average Investor

$20,000

40/60 Stock/Bond Fund

$35,000

S&P 500

$61,000

I encourage investors to be patient, methodical, and mostly ignore recent performance – good or bad. This same advice applies whether you are investing in short-term treasury funds, stock index funds, or our algorithms. Investment decisions should be based primarily on when you plan to spend the money and your risk tolerance, not on recent performance – good or bad.

Good News for Your Shorter-Term Savings!

Interest rates are much higher than they have been in the last 10 years, but many banks aren’t going to automatically raise the interest rate you get on your savings. So, action may be needed. One to three month US treasury funds are yielding over 5% and can be purchased in most brokerage accounts including Interactive Brokers via Tines Capital. If you don’t feel comfortable purchasing them on your own and saving yourself the Tines Capital management fee, we are happy to help you do it!

Some local banks have savings rates that are paying as little as 0.25% (Arvest and BOK). One solution is to find other banks with better rates or shop for a certificate of deposit (CD) which are paying closer to the 4-5% range. These can be good since they lock in a rate but remember that you must make sure the lockup period on a CD works well for your situation.

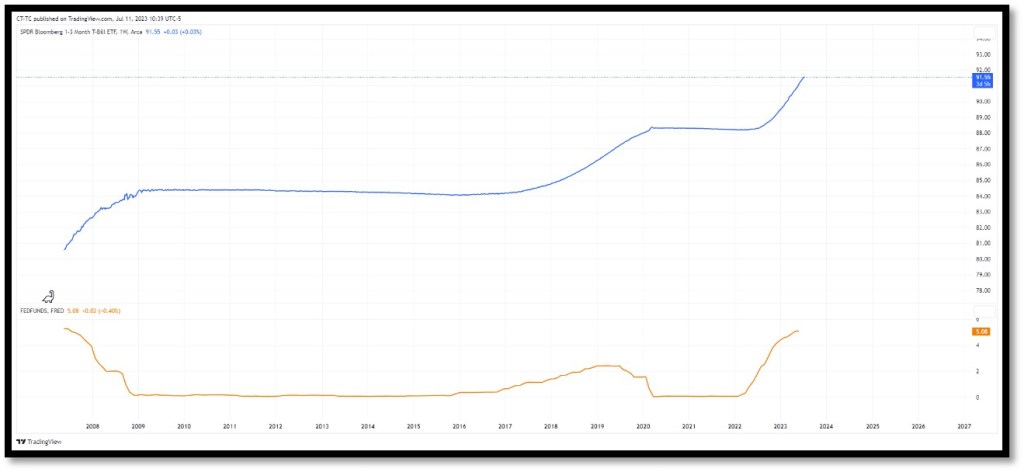

In the chart below the Federal Funds interest rate is shown in orange. When the Federal Funds rate goes up the cost of all debt tends to go up. This is great for savers since when you deposit money in a bank you are in a way loaning them money. Likewise, treasuries are essentially loans you give the US government that obligate the government to pay interest to you. They can also be bought and sold any day the market is open making them much more liquid than a CD.

The volatility in short-term treasury funds is extremely low as you can see by the smoothness of the blue line in the chart. For 2009-2017 and 2020-2021 the fund was slightly negative because interest rates were near zero and slightly below the management fee of the fund. If rates drop lower than the management fee it can become advantageous to sell treasury funds and convert to cash or another investment. Currently, short-term treasury funds are growing at a rate of about 5% – including dividends. If the Fed raises rates, we could see the growth steepen. If they drop rates, we could see the growth rate of these funds flatten. Either way if you have significant cash-like savings you should be trying to get around 4-5% in this current environment.

Mailing Addresses

Now that the second quarter has ended you should be seeing quarterly statements in the mail in the coming weeks. If you do not receive your statement(s) please double check that you have the correct home and mailing address on file with interactivebrokers.com. If you would like any help, remember that you can always reach out to Tines Capital anytime for help or questions.

Disclaimer

Disclaimer Tines Capital, LLC (“TC”) is a registered investment adviser in the State of Oklahoma and in other jurisdictions where exempted. The information on this website, including videos, articles, tools, and other materials, is for educational and informational purposes only. It is not intended as investment, tax, accounting, or legal advice, nor should it be relied upon as the sole basis for any financial decision.

Viewing this content, submitting information, or using any linked tools (including RightCapital) does not create an advisory relationship with TC. An advisory relationship is established only after you and TC enter into a signed written agreement.

Past performance is not indicative of future results. Investing involves risk, including possible loss of principal. TC makes no guarantees as to the accuracy, timeliness, or completeness of the information provided, which is offered “AS IS” without warranty of any kind. TC disclaims all warranties, express or implied, including but not limited to warranties of merchantability, non-infringement, and fitness for a particular purpose.

Links to third-party sites or tools are provided for convenience only. TC does not control and is not responsible for the content, security, or privacy practices of these third parties. Your use of any third-party website or tool is at your own risk and subject to its own terms and privacy policy.