The following videos and discussion will give you an overview of how Tines Capital looks at leveraged investing and why we think it can be such a powerful tool.

Videos

If you prefer to watch these videos on YouTube there is a playlist for them here: https://www.youtube.com/playlist?list=PLvVxU7oh9gT2TRkovQfiq-V3gv6VrAHzO

Applying Leverage to the Stock Market

Tactical Trading

Diversification

Leverage Diversification and Tactical Trading

2X Stocks or Cash?

2X Stocks or 1X Stocks?

3X, 2X, or 1X Stocks?

The Case for Tines Capital Leveraged Strategies

At Tines Capital, our approach to leveraged investment strategies is built on a simple hypothesis: leverage, when applied within a diversified, rules-based framework and managed with discipline over time, can improve capital efficiency without abandoning risk control.

We pair these strategies with comprehensive financial planning, tax-efficient account structures, and personalized goals to help investors manage risk, stay disciplined, and make their capital work harder.

Suitability Note: Due to the nature of leverage, these investment strategies may not be appropriate for all investors.

Table of Contents

- The Case for Tines Capital Leveraged Strategies

- Why Leverage Gets a Bad Rap

- Historical Leverage Simulation

- How to Harness Leverage

- Lessons from History: Why a Long-Term Perspective Matters

- Exploring Non-Traditional Assets

- The Tines Capital Leveraged Strategy Performance

- What This Means for Investors

- Why IRAs Are Ideal for Leveraged Strategies

- Tailored Strategies for Every Investor

- Conclusion

- Disclaimer

- Appendix A

Key Takeaways (TL;DR)

- Leverage is a tool. Leverage allows investors to control a larger asset with a smaller amount of capital. Think of a mortgage. Importantly, the type of leverage we recommend for investment accounts does not require taking on personal debt. Used thoughtfully, it can amplify returns while keeping risk manageable.

- Diversification is key. Using leverage increases volatility, so spreading exposure across multiple assets is even more important. Diversification helps smooth out market swings and protect capital.

- Rules beat guesses. Tactical adjustments to leverage can be beneficial, but they work best when guided by mathematical, rules-based indicators rather than news headlines, forecasts, or hunches.

- Think long-term. Giving a strategy time to work allows short-term fluctuations to smooth out and lets compounding do its work. Patience is critical.

- Built on a foundation of planning. Tines Capital combines these strategies with fiduciary financial planning and expert tools to help clients take on the right level of risk for their goals.

- Qualified accounts enhance efficiency. Using a Roth or Traditional IRA account structure can help minimize short term and long term tax drag, letting your leveraged strategy compound more efficiently.

- Each investor is unique. Leveraged strategies can be customized to fit different goals and risk tolerances. Strategies can vary in complexity and can be deployed to pursue higher growth over decades, or structured for capital preservation.

Building on a Strong Foundation

Every investor we work with starts with the same basic question: “How can I grow my money without taking on too much risk?”

The answer always begins with the same principles: live below your means, save consistently, diversify, keep fees low, and stay invested. These principles have helped countless people build wealth, and they form the foundation of every portfolio we build.

At Tines Capital, we believe leverage is an underutilized tool that can help strengthen returns while staying aligned with those same principles. It’s not about chasing big, risky bets. It’s about applying discipline, rules, and measured exposure to capture more of what the market already offers. In the sections that follow, we’ll break down how we design our leveraged strategies and how they can fit into an investors long-term wealth-building strategy.

The Two Paths Investors Take to Potentially Increase Returns

When investors look to increase returns, there are generally two approaches they take: concentration or leverage. Each can deliver meaningful upside, but each also carries significant risks. Understanding both is essential before deciding which, if either, fits your portfolio.

Concentration: The “All or Most Eggs in One Basket” Approach

Concentration means putting more of your capital into fewer investments. That could mean focusing on U.S. stocks instead of global markets, or picking one or a handful of individual companies rather than a broad index.

Example 1 – Sector Concentration (Jul 2008 to Dec 2025)

Example 1 Details: Portfolio Visualizer, retrieved Jan 2026. Returns are nominal (not inflation-adjusted) and include the reinvestment of dividends where applicable. Performance figures are net of underlying ETF expenses but gross of advisory fees, as this illustration represents market data and not a managed portfolio strategy.

In this period, concentrating further into U.S. stocks (VTI) outperformed global markets (VT). Pushing the concentration one step further into a single sector like U.S. technology (VGT) delivered even stronger results. This is a positive example of concentration working out. But it’s also a reminder that such results depend entirely on choosing the right area ahead of time.

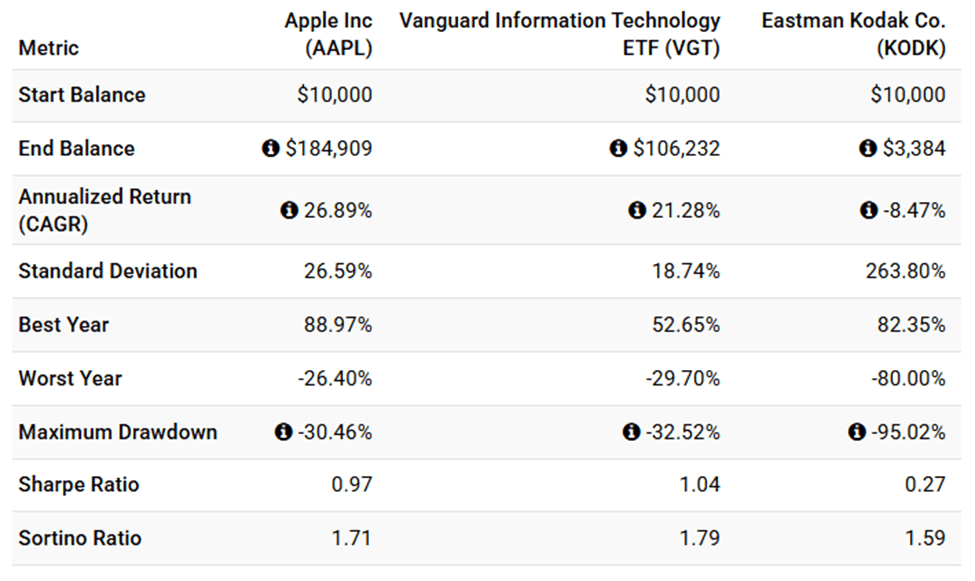

Example 2 – Individual Stock Concentration (Oct 2013 to Dec 2025)

Example 2 Details: Portfolio Visualizer, retrieved Jan 2026. Returns are nominal (not inflation-adjusted) and include the reinvestment of dividends where applicable. Performance figures are net of underlying ETF expenses but gross of advisory fees, as this illustration represents market data and not a managed portfolio strategy.

This example highlights the double-edged nature of concentration. Moving from a diversified tech ETF like VGT into a standout performer such as Apple would have meaningfully boosted returns. But the same act of concentration could just as easily have gone the other way. Allocating heavily to a company like KODK would have likely been disappointing.

Many investors are tempted by a strong-performing sector or stock and *especially* by recent strong performance (recency bias), but decades of research show that consistently picking winners is extremely difficult, which is where concentration falls short.

At Tines Capital, our view is that broad diversification is generally a more reliable path to long-term wealth than concentration. Diversification systematically reduces avoidable risks and increases the likelihood of capturing market growth over time.

As Harry Markowitz famously noted, diversification is the only “free lunch” in investing.

Leverage: Amplifying Exposure

The second path to higher returns is leverage. Most people are familiar with leverage through mortgages. A relatively small down payment gives you exposure to a much larger asset. In investing, leverage works the same way.

There are multiple ways to achieve leverage: personal loans, margin accounts, home equity lines, futures, and options. Each of these options comes with borrowing costs, operational complexity, and liquidity risk. Mistakes, market swings, or a liquidity squeeze can dramatically magnify losses, and the investor is personally liable for the debt. Not everyone is suited for this.

Leveraged ETFs (or LETFs) provide an alternative to the other methods mentioned above. LETFs handle borrowing, derivatives, and daily rebalancing automatically, with costs included in the expense ratio. While simpler and less personally risky than taking on debt yourself, LETFs have limitations. Daily compounding and volatility decay can cause long-term returns to deviate from the target multiple, even if the underlying index ends flat.

At Tines Capital, we generally advocate against taking on personal debt to achieve leverage. Borrowing through a personal loan, home equity line, or margin account makes you personally liable for repayment, regardless of how your investments perform. By contrast, some investment vehicles embed leverage within the product itself (such as LETFs, futures, or options) allowing you to amplify market exposure while limiting risk strictly to the capital invested.

Why Leverage Gets a Bad Rap

As engineers turned advisors, the word “leverage” never carried the negative connotation it might for some. We know a lever doesn’t create force; it redistributes it. Used correctly, it can make something heavy lighter and safer. Used incorrectly… it can be dangerous.

Financial leverage works the same way.

When leverage is paired with risky concentrated bets, short-term speculation, short time horizons, high levels of personal debt, or lack of liquidity, things can break quickly. That’s the version of leverage most people remember from the 2008 financial crisis and the dot-com bust. Excessive borrowing and overconcentrated bets can quickly turn into a disaster.

The Tines Capital approach to leveraged strategies is something entirely different. It isn’t about swinging for the fences (#yolo) or chasing quick gains. It’s about applying a measured amount of extra exposure across a diversified portfolio and adjusting that exposure when conditions become less favorable. Think of it more like fine tuning a volume dial than flipping an on-off switch.

Leverage isn’t a magic solution. It’s not right for every situation, but it can be a useful tool in a variety of different portfolios. In the sections that follow we will discuss some of the methods we use to help harness leverage into a powerful force for your portfolio.

Even legendary investors use leverage in structured ways. At Berkshire Hathaway, Warren Buffet used insurance premiums to act as low-cost leverage. “Buffett’s Alpha” estimates this gives Berkshire an effective 1.6X leverage at a cost lower than the Treasury bill rate. It’s a brilliant example of practical leverage.

Historical Leverage Simulation

Before diving into returns, it’s important to understand volatility decay and how it can affect leveraged investments.

Volatility decay occurs because losses require proportionally larger gains to recover. For example, if an unleveraged $10,000 investment drops 5% to $9,500, it takes a 5.26% gain to break even ($9,500 × 1.0526 ≈ $10,000). A 2X leveraged ETF in the same scenario would fall 10% to $9,000, requiring an 11.1% gain to recover ($9,000 × 1.111 ≈ $10,000).

Volatility decay is a short-term, path-dependent phenomenon: leveraged positions lose value faster during choppy or sideways markets because losses require proportionally larger gains to recover. This effect is strongest when prices fluctuate frequently but don’t trend strongly in one direction. For instance, during the COVID-19 market crash, the S&P 500 was roughly flat from January to August 2020, and a 3X leveraged investment in the S&P 500 ended up down ~30%.

Long-term appreciation helps offset this because, over time, a consistent upward trend allows the leveraged position to grow despite intermittent volatility. Even with volatility decay, sustained positive returns compound and can outweigh the temporary drag.

Volatility decay doesn’t disappear; it just becomes less relevant when the underlying asset has a strong, persistent upward trajectory. Leveraged ETFs or strategies still experience extra drawdowns and more volatile swings, but patient investors in appreciating markets are more likely to see positive long-term outcomes.

The charts and table below shows the simulated performance with leverage.

Hypothetical & Simulated Performance Notice:

- Not Actual Results: The performance shown is backtested, hypothetical, and does not represent actual client accounts or trading.

- Simulated Leverage: Leveraged ETFs did not exist for the majority of the illustrated time periods. Simulated 2X and 3X leverage is synthetically constructed using a strict data hierarchy (Actual ETFs > Mutual Funds > Market Indices) and explicitly subtracts estimated borrowing costs and ETF expense spreads.

- Fees: Returns for the simulated strategies are presented NET of an assumed 2% annual advisory fee. Comparative benchmark indices are presented GROSS of advisory fees.

- Please see the “Methodology & Disclosures” section at the end of this document for critical details regarding the data construction hierarchy, hindsight bias, and risks of volatility decay.

These simulations illustrate the double-edged nature of leverage. While 3X leverage can dramatically amplify long-term returns as shown over this period, it also produces extreme peaks and valleys along the way (including a ~92% drawdown and 6 years underwater).

How to Harness Leverage

So, now that we’ve seen how leverage can enhance returns, the question becomes: how can investors harness this potential responsibly?

At Tines Capital, we approach the design of our leveraged strategies with three complementary mechanisms:

- Diversification Across Asset Classes

Concentrated leverage can be catastrophic in the event of a market shock. By distributing exposure across different asset classes such as equities, bonds, precious metals, cash equivalents, and non-traditional assets, we reduce the likelihood that a single drawdown overwhelms the portfolio. Historical data show that broad diversification significantly mitigates the effect of severe market corrections. - Tactical Risk Management

Our system continuously monitors market volatility, trend indicators, and risk-adjusted signals. When risk rises or volatility spikes, leverage is automatically reduced according to predefined rules. Conversely, when conditions stabilize, leverage may be increased to capture upside opportunities. These adjustments are systematic, not discretionary, helping prevent emotional decision-making from impacting performance. - Commitment to a Long-Term Horizon

Leveraged positions increase volatility. By committing capital for a long-term horizon investors allow temporary swings to normalize and benefit from the underlying growth of appreciating assets. Historical simulations show that, even with periodic drawdowns, disciplined leveraged strategies have historically outperformed non-leveraged equivalents over extended periods.

Controlling leverage doesn’t eliminate risk, but it does attempt to manage it intelligently. By combining diversification, tactical adjustments, and a long-term horizon, we seek to preserve capital during drawdowns while capturing the upside potential of leverage.

Lessons from History: Why a Long-Term Perspective Matters

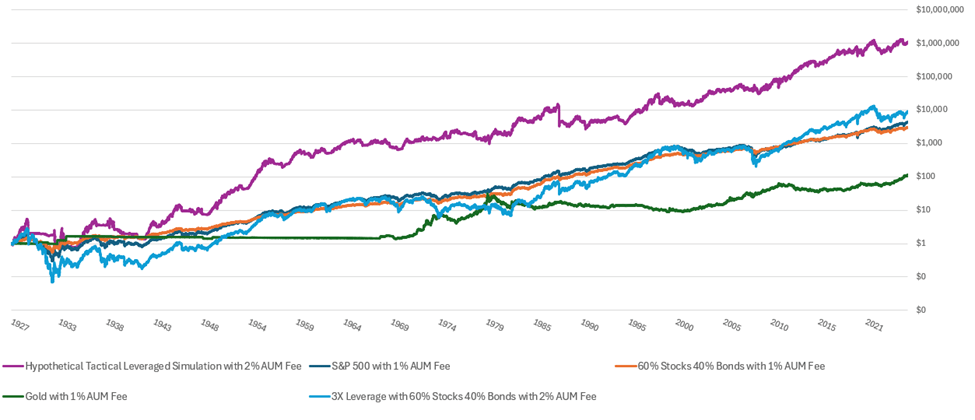

Let’s explore how a very simple, tactical, leveraged strategy might have performed from 1927 to today. Even though this example backtested strategy is straightforward (details below), it follows the same underlying principles we emphasize at Tines Capital: diversification, tactical adjustments, and a long-term horizon.

The results are striking. Over this extended timeframe, a disciplined leveraged approach in this hypothetical example has historically delivered significantly higher annualized growth than the S&P 500 alone, and yet at the same time, the backtest highlights the natural volatility of leverage. Drawdowns occur, sometimes sharply, sometimes prolonged and brutal, again reinforcing why patience, rules-based management, and a long-term perspective are essential.

Hypothetical & Simulated Performance Notice:

- Not Actual Results: The performance shown is backtested, hypothetical, and does not represent actual client accounts or trading.

- Simulated Leverage: Leveraged ETFs did not exist for the majority of the illustrated time periods. Simulated 2X and 3X leverage is synthetically constructed using a strict data hierarchy (Actual ETFs > Mutual Funds > Market Indices) and explicitly subtracts estimated borrowing costs and ETF expense spreads.

- Fees: Returns are presented NET of an annual advisory fee..

- Please see the “Methodology & Disclosures” section at the end of this document for critical details regarding the data construction hierarchy, hindsight bias, and risks of volatility decay.

Exploring Non-Traditional Assets

The previous section illustrates the strength of leverage when it’s applied in a thoughtful way. At Tines Capital, we also provide clients with the option to incorporate additional non-traditional assets as diversifiers in our Leveraged and Non-Traditional Asset Strategy. Two key examples are volatility products and cryptocurrency.

Volatility products function like market “insurance.” Investors can sell insurance (i.e., collecting premiums during calm or sideways markets) to generate returns, or buy insurance to protect against sharp market declines when turmoil is expected. These products are highly dynamic and can move dramatically overnight, so they carry significant risk. However, when used thoughtfully, they can serve as a valuable diversifier.

Cryptocurrency offers another layer of diversification. While it has increasingly shown periods of correlation with equities (particularly during broad liquidity-driven market cycles) it remains structurally different from traditional stocks and bonds. At the same time, cryptocurrency markets are highly volatile and can experience extreme swings, so any allocation should be approached with caution and risk management in mind.

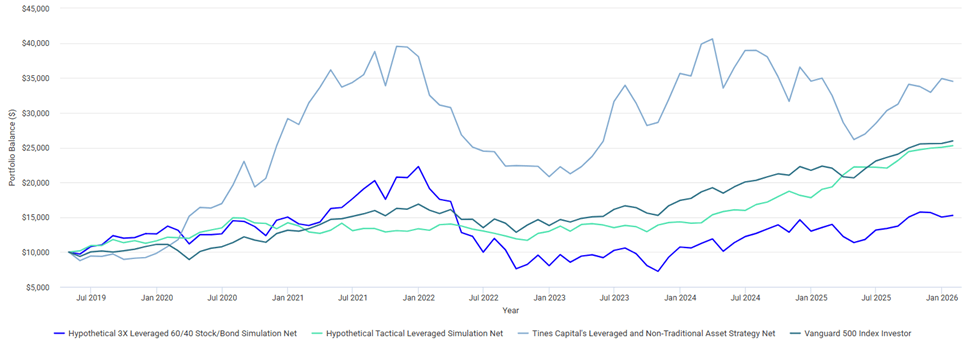

The Tines Capital Leveraged Strategy Performance

Alright, enough about the hypothesis. What do the results actually look like?

The performance of any strategy is best understood in the context of real markets, real drawdowns, and real investor experience.

Since April 23, 2019, a hypothetical $10,000 investment in the Tines Capital Leveraged and Non-Traditional Asset Strategy has grown to $31,044, delivering a 19% annualized return.

The cumulative return chart shows the journey: a rapid rise to 300% by October 2021, a valley lasting until April 2024, followed by a recovery close to the all-time high, and then a pullback through October 2025. This pattern highlights both the volatility inherent in leveraged strategies and the potential reward for investors who remain patient and disciplined.

Proprietary Live & Simulated Performance Notice

- Live Performance (Roth IRA): The “Leveraged Algorithm” began signaling on April 23, 2019. Results from this date through 4/30/2019 reflect actual trades executed in a personal, tax-advantaged Roth IRA belonging to the portfolio manager, prior to the formation of the advisory firm. It does not represent third-party client assets.

- Simulated Baselines: The “Hypothetical 3X” and “Tactical Leveraged Simulation” lines are purely hypothetical backtests utilizing simulated leverage data.

- Fees: Both the proprietary live strategy and the simulations are presented NET of a hypothetical 2.00% annual advisory fee (as no actual fee was charged to the personal account).

- Please see the “Methodology & Disclosures” section at the end of this document for critical details regarding the data construction hierarchy and limits of proprietary performance.

What This Means for Investors

At Tines Capital, success with leveraged strategies comes down to balancing growth potential with disciplined risk management. The cumulative performance chart and table illustrate this clearly: volatility is inevitable, but a diversified, rules-based approach helps investors stay invested through the market’s peaks and valleys, allowing compounding to work in their favor. While it’s tempting to chase recent winners, adhering to a tactical, rules-driven methodology gives the best chance to capture long-term uptrends while managing drawdowns effectively.

Why IRAs Are Ideal for Leveraged Strategies

Passive index funds are generally tax-efficient because they trade infrequently and distribute minimal capital gains each year.

By contrast, a leveraged or tactical strategy—like the one we’ve been discussing—trades more actively. That means gains are often realized and taxed in the year they occur, which can materially reduce after-tax returns, especially for investors in higher brackets.

The solution is asset location. Strategies that generate frequent taxable gains are often better suited for tax-advantaged accounts such as IRAs, Roth IRAs, HSAs, or certain charitable structures. Meanwhile, highly tax-efficient index funds can remain in taxable accounts with minimal drag.

Putting an actively traded strategy in a taxable account while sheltering passive index funds inside retirement accounts is like parking your Ferrari F80 on the street and keeping your 2000 Chevy Cavalier in the garage.

Park the Ferrari in the garage!

Benefits of Qualified Accounts (Traditional or Roth)

- Trades inside the account are not subject to capital gains taxes, allowing for frequent rebalancing without eroding returns. However, please note that taxes may be incurred once assets are withdrawn from the account.

- Dividend and interest income compounds without immediate tax consequences.

- Contribution limits are structured to encourage long-term saving, aligning naturally with the extended time horizon needed for leveraged strategies.

Traditional IRA Specific Benefits

- There is no income limit to make a non-deductible contribution to a Traditional IRA.

- Contributions may be tax-deductible, providing an upfront tax benefit and reducing current-year taxable income.

Roth IRA Specific Benefits

- There are income limits on who can directly contribute to a Roth IRA but investors can typically fund a Traditional IRA then move the funds to a Roth IRA (Roth Conversion or Backdoor Roth).

- Contributions grow tax-free, and qualified withdrawals of both contributions and earnings are completely tax-free.

- Contributions can be withdrawn at any time!

- No required minimum distributions, allowing leveraged positions to compound for decades without forced liquidation.

- Beneficiaries inherit the portfolio tax-free, making Roth IRAs a highly efficient vehicle for passing wealth to the next generation.

At Tines Capital, we view qualified accounts like Traditional and Roth IRAs as ideal foundations for disciplined, long-term leveraged strategies. By combining the tax advantages, flexibility, and compounding benefits of these accounts with a carefully structured approach to leverage, investors can pursue enhanced returns while managing risk, maintaining liquidity, and keeping taxes under control. In short, these accounts provide a powerful, efficient framework for capturing upside potential responsibly and sustainably.

Tailored Strategies for Every Investor

At Tines Capital, we recognize that every investor is unique. Our leveraged strategies aren’t one-size-fits-all and they can be customized to fit different goals, time horizons, and risk tolerances.

Some investors may prioritize long-term growth, deploying strategies designed to maximize compounding over decades. Others may focus on capital preservation, structuring leverage carefully to limit drawdowns and maintain stability. Strategies can also vary in complexity, from simpler, rules-based approaches to more sophisticated allocations that include non-traditional assets.

A key benefit of working with Tines Capital is that these strategies are integrated with fiduciary guidance, financial planning software, and comprehensive tools. This ensures each strategy is aligned with the investor’s goals, risk comfort, and overall financial plan, providing a fully customized, client-centric approach to pursuing growth while managing risk.

Conclusion

We think leverage is like a tool in your toolbox and it works best when paired with diversification, rules-based tactics, and a long-term mindset. Combine that with fiduciary planning, smart account structures, and strategies tailored to your goals, and you’ve got a way to manage risk, stay disciplined, and make your capital work harder.

If you want to learn about our leverage strategies and how they might fit into your portfolio, reach out to us at info@tinescapital.com or visit or website tinescapital.com/contact.

Disclaimer

The information presented herein is for educational and illustrative purposes only and does not constitute investment advice, an offer to sell, or a solicitation to buy any securities. Past performance is not indicative of future results. All examples, backtests, charts, and simulations—including those using historical price data, interpolated data (daily, weekly, or monthly), or synthetic leveraged return estimates in periods where actual 3× ETF data did not exist—are hypothetical and do not reflect actual client performance. Hypothetical results have inherent limitations, are designed with the benefit of hindsight, and may not account for real-world market conditions, liquidity constraints, trading costs, taxes, or behavioral factors that can materially affect outcomes.

Leveraged ETFs carry unique risks, including volatility decay, compounding effects, and potentially significant short-term drawdowns. The modeled strategies discussed may behave differently in live market conditions, and there is no guarantee that any investment strategy—leveraged or otherwise—will achieve its stated objectives or avoid losses.

All investments involve risk, including the potential loss of principal. Investors should consider their own financial situation, risk tolerance, and investment objectives before implementing any strategy. Tines Capital does not guarantee the accuracy or completeness of the information contained in this document, which is subject to change without notice. For personalized advice, please consult with a qualified financial professional.

Appendix A

The Synthetic Leverage Data Hierarchy

Because the simulations in this document span decades prior to the existence of leveraged ETFs, a strict data hierarchy was required to construct the 2X and 3X leveraged exposure. This hierarchy is applied uniformly to all long-term simulations presented herein:

- Actual Leveraged ETFs: When available, actual historical daily price data for leveraged ETFs (e.g., UPRO for equities and TMF for bonds) was utilized.

- Simulated Leverage via Mutual Funds: Prior to the inception of these ETFs, actual unleveraged mutual fund data (Vanguard 500 Index [VFINX] and Vanguard Long-Term Treasury [VUSTX]) was utilized. Leverage was simulated by mathematically amplifying daily returns.

- Synthetic Leverage via Market Data: For periods prior to the inception of VFINX and VUSTX (e.g., back to 1927), equity returns were synthetically constructed using S&P 500 (SPX) price data combined with S&P 500 Dividend Yield by Month. Bond exposure was synthetically constructed using historical 10-year U.S. Treasury yields. If daily data was unavailable, a “step-forward” approach was used, carrying the most recent monthly price forward until a new price was published.

Accounting for Borrowing Costs & Fees All simulated leveraged periods strictly account for the internal cost of leverage. Borrowing costs were calculated by subtracting the Federal Funds rate (or the 3-Month Treasury Bill rate, depending on historical availability) plus an additional spread to approximate the embedded costs typically incurred by modern leveraged ETFs. Furthermore, simulated strategy returns are presented NET of an assumed maximum advisory fee (detailed under each chart), while comparative indices are presented GROSS of advisory fees. All assets assume the reinvestment of dividends.

Strategy Methodology & Backtest Assumptions

Data Sourcing and Pricing

- Start Date: December 30, 1927. This date was selected based on the earliest available daily pricing data for the S&P 500 Index via TradingView.

- Asset Coverage: The backtest evaluates the S&P 500 (Total Return, assuming all dividends are reinvested), Bonds, and Gold.

- Data Interpolation: Where daily pricing was historically unavailable for an asset (e.g., historical Gold prices that were only published monthly), the model uses a “step-forward” approach. The most recent available price was carried forward for each daily observation until a newly published price became available.

Portfolio Allocation & Algorithmic Decision Rules The portfolio consists of a permanent 1% cash allocation and two distinct algorithmic sleeves, each representing 49.5% of the total portfolio. Both sleeves utilize a 200-day moving average (200-DMA) to determine market trends. Trend signals are evaluated only once per month, on the last trading day of the month.

- Permanent Allocation (1%): Held constantly in Cash.

Sleeve 1: Dynamic Multi-Asset Trend (49.5% Allocation) This portion of the portfolio evaluates assets in a strict hierarchy. On the last trading day of the month, the algorithm allocates 100% of this sleeve’s capital to the first asset in the following sequence that is trading above its 200-DMA:

- 3x Leveraged Equities: If trading above its 200-DMA, hold 3x Leveraged Equities.

- 3x Leveraged Bonds: If Condition 1 fails, but 3x Leveraged Bonds are trading above their 200-DMA, hold 3x Leveraged Bonds.

- 1x (Unleveraged) Gold: If Conditions 1 and 2 fail, but Gold is trading above its 200-DMA, hold 1x Gold.

- Cash: If all three assets are trading below their respective 200-DMAs, hold Cash.

Sleeve 2: Leveraged Equity/Bond Toggle (49.5% Allocation) This portion of the portfolio is designed to remain fully invested in leveraged assets at all times, toggling between equities and bonds based on the equity trend:

- Positive Equity Trend: If 3x Leveraged Equities close the month above their 200-DMA, this sleeve is 100% invested in 3x Leveraged Equities.

- Negative Equity Trend: If 3x Leveraged Equities close the month below their 200-DMA, the sleeve shifts entirely to 3x Leveraged Bonds.

Website Disclaimer

Tines Capital, LLC is an Investment Advisor registered with the State of Oklahoma. All views, expressions, and opinions included in this communication are subject to change. This communication is for informational purposes only and is not intended as tax, accounting or legal advice, as an offer or solicitation of an offer to buy or sell, or as an endorsement of any company, security, fund, or other securities or non-securities offering. This communication should not be relied upon as the sole factor in an investment making decision.

Past performance is no indication of future results. Investment in securities involves significant risk and has the potential for partial or complete loss of funds invested. It should not be assumed that any recommendations made will be profitable or similar to the performance noted in this publication.

The information herein is provided “AS IS” and without warranties of any kind either express or implied. To the fullest extent permissible pursuant to applicable laws, Tines Capital, LLC (referred to as “TC”) disclaims all warranties, express or implied, including, but not limited to, implied warranties of merchantability, non-infringement, and suitability for a particular purpose.

All opinions and estimates constitute TC’s judgment as of the date of this communication and are subject to change without notice. TC does not warrant that the information will be free from error. The information should not be relied upon for purposes of transacting securities or other investments. Your use of the information is at your sole risk.

Under no circumstances shall TC be liable for any direct, indirect, special or consequential damages that result from the use of, or the inability to use, the information provided herein, even if TC or a TC authorized representative has been advised of the possibility of such damages. Information contained herein should not be considered a solicitation to buy, an offer to sell, or a recommendation of any security in any jurisdiction where such offer, solicitation, or recommendation would be unlawful or unauthorized.